Protect & Secure Your Family's Future

Over 300 5-Star Reviews!

Our Commitment in Action

Explore our journey of protecting businesses with reliable and comprehensive insurance solutions. From small enterprises to large corporations, we safeguard what matters most. See how we make a difference!

Elite Coverage Options for Limitless Security

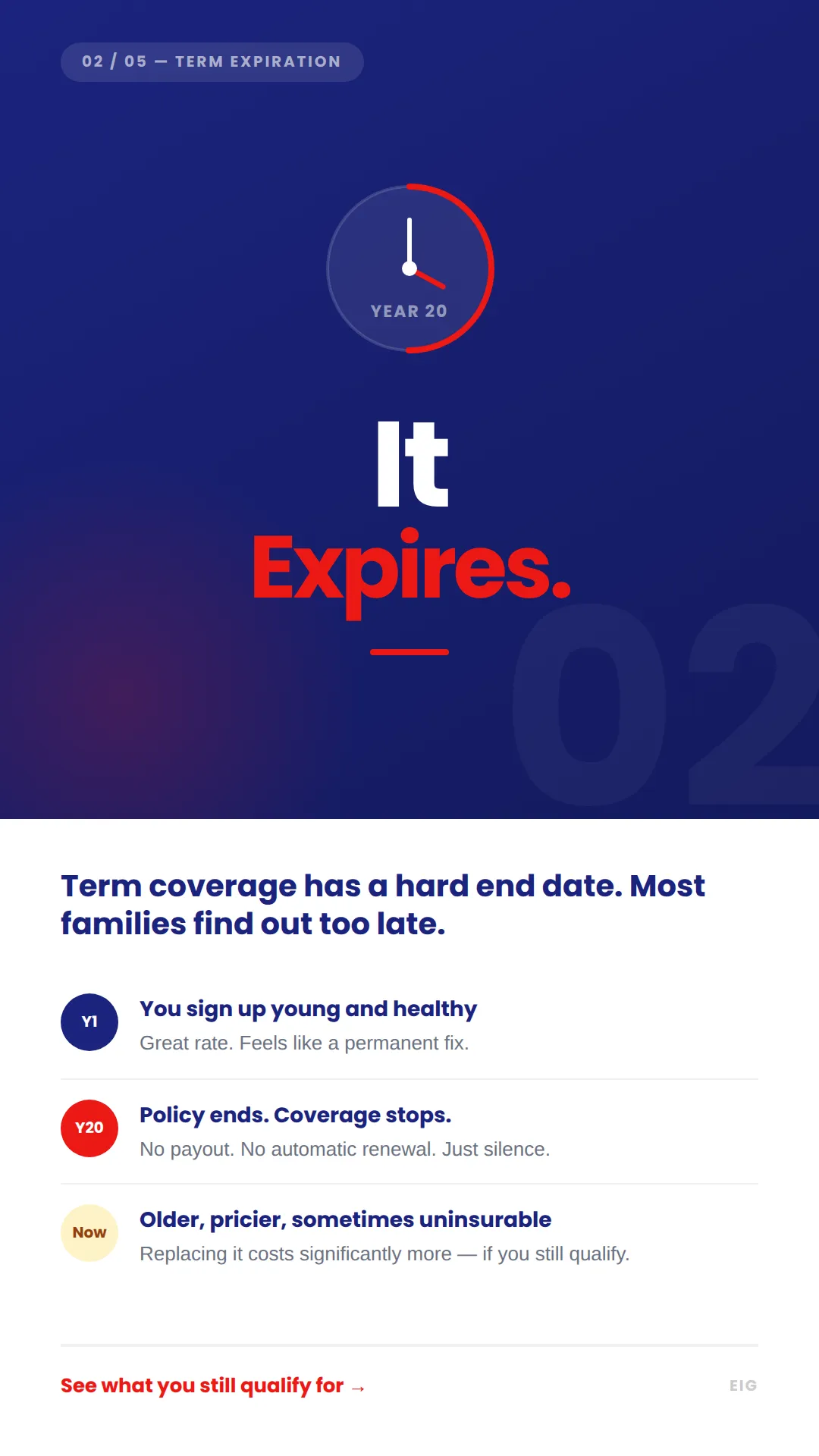

Final Expenses

A small whole life policy built to cover funeral and burial costs — typically $10,000 to $30,000 — so your family isn't left covering that bill during an already hard time. Often available with no medical exam.

Mortgage Protection

Independent term life coverage sized to your mortgage balance or monthly payments, so your family isn't forced to sell the home if something happens to you. This is not a lender product required to close your loan.

Living Benefits

Most policies we place let you access part of your death benefit early if you're diagnosed with a serious critical, chronic, or terminal illness — turning an "if I die" policy into one that also helps pay bills if you get sick.

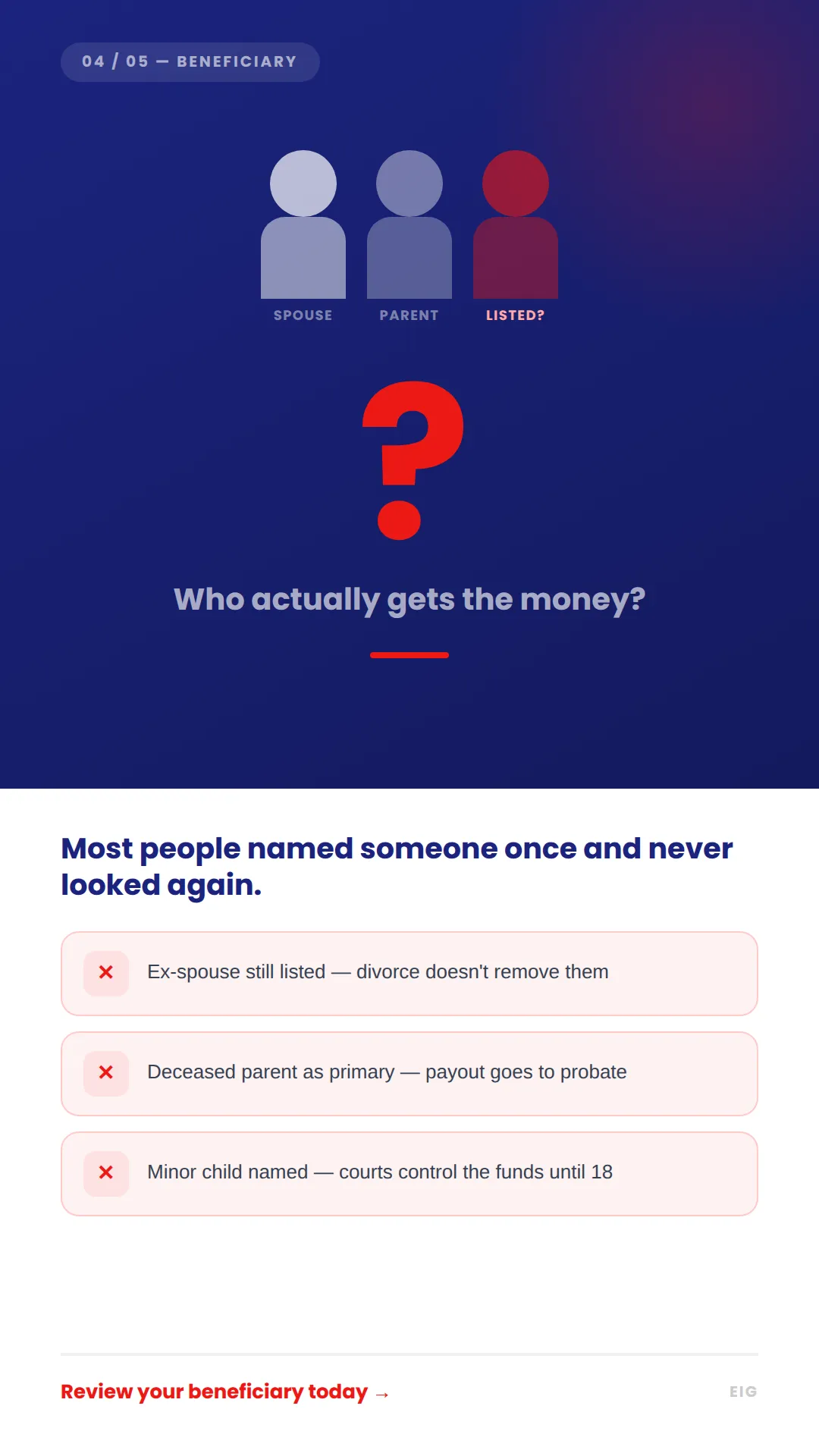

Already Have Life Insurance? Identify The Gaps.

Most coverage gaps aren't discovered until a claim gets denied or a policy lapses unexpectedly.

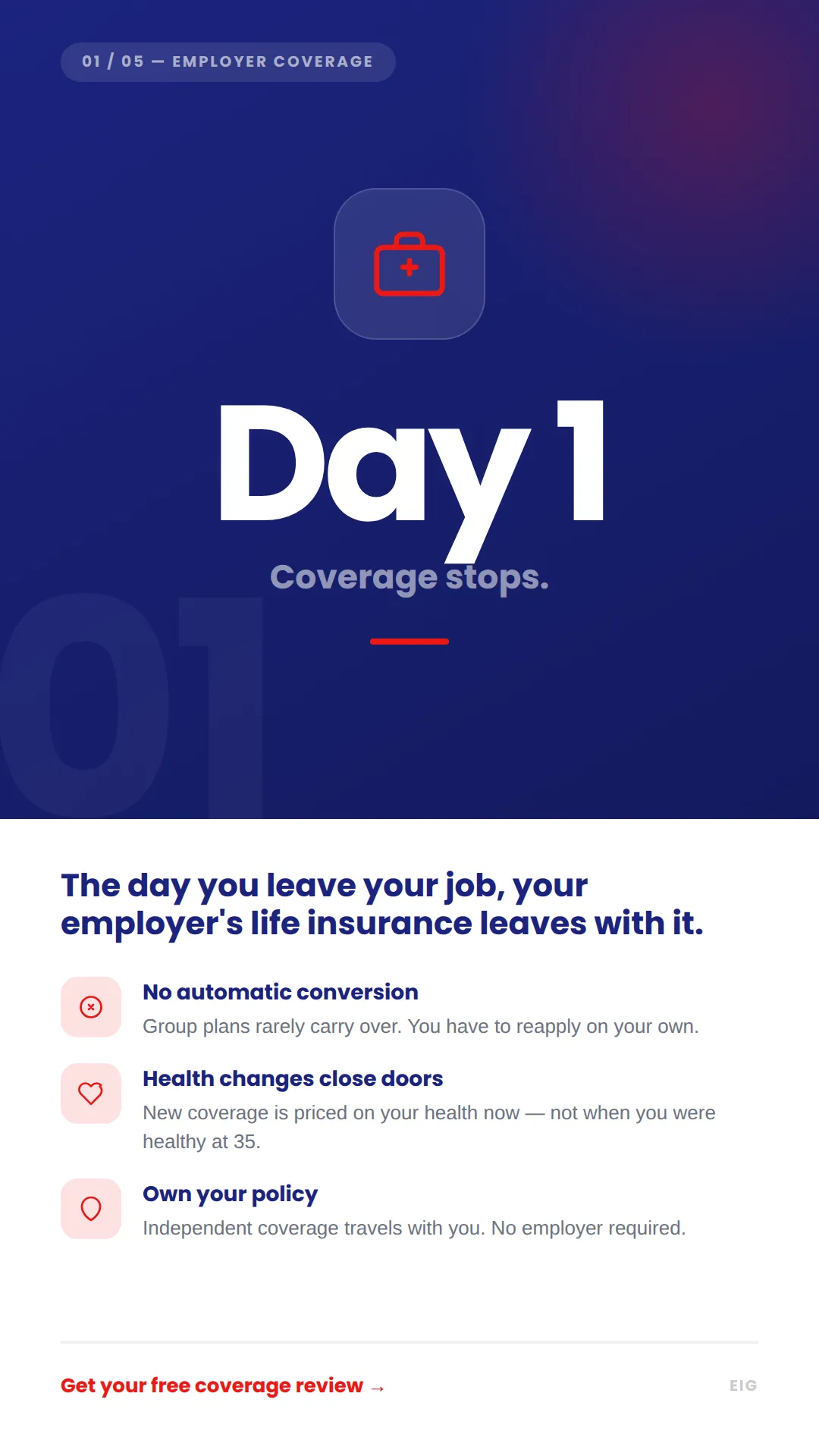

A policy from a few years ago doesn't always hold up: employer coverage disappears the day you leave that job, term policies have a hard expiration date, and older policies often don't include the living-benefits newer ones provide. Pricing might be an issue too — are you certain your agent reviewed all the options with you or just the one that paid them the most commission? A free review tells you exactly where you stand, with zero obligation to change anything.

Why Families Trust Me

Customized Coverage Plans

I compare your situation against multiple A-rated carriers instead of fitting you into one company's product. What you end up with is built around your actual budget and family's needs, not a one-size-fits-all policy.

No-Pressure Conversations

You'll get straight answers about what coverage actually costs and covers — no countdown timers, no "today only" pricing. Move forward when you're ready, or don't; the conversation costs you nothing either way.

Transparent Pricing and Solutions

I walk you through exactly what affects your price — age, health, coverage type — before you ever apply, so underwriting doesn't surprise you. We're not chasing the cheapest policy on the shelf; we're finding the one that actually holds up when your family needs it.

Independent Agent

I'm not tied to one insurance company, so I'm never stuck pushing one specific product when it's not the right fit. That means real comparisons and real recommendations based on what works for your family — not a sales quota.

Secure Your Families Future, Worry-Free

Meet Your Licensed Agent

Bradley Vazquez

Before insurance, Brad spent years as a marketing consultant — which means he's seen how sales gets done across a dozen industries, including the parts nobody loves. That's exactly why he runs the opposite way: no pressure, no scripts, just a straight answer about what actually fits your situation. Brad sees this work as more than a paycheck — guided by faith and a genuine sense of higher purpose in helping families get this right, and that's the standard every conversation gets held to.

Frequently Asked Questions

Will going through an independent agency cost me more?

No — carriers set rates the same way whether you buy direct or through an agent. The difference is I compare multiple insurance companies for you instead of you being locked into whichever one company you called first.

How is this different from buying through a call center?

You're talking directly to me — a licensed agent who knows your file — not a rotating queue. And because I'm contracted through multiple carriers as an independent agent, if one carrier's underwriting doesn't fit your health or budget, I can move to another without a hassle.

Do I need a medical exam?

Depends on the policy. Many term and final-expense options skip the exam entirely. I'll tell you upfront which path fits before you apply for anything.

When is the best age to get life insurance?

The honest answer: younger is almost always cheaper, but the best age is whatever age you are TODAY. Premiums are priced on two things — your age and your health — and both tend to work against you every day that goes by. A healthy 30-year-old will lock in a significantly lower rate than the same person at 45 with a few health changes on their record. That said, I work with clients across a wide range of ages, and having coverage later is still better than having none at all. The question worth asking isn't "am I too old?" — it's "what's available to me right now?" That's exactly what a 10 min call with me answers.

What happens if me and/or my family needs to file a claim?

You can call me directly. After your application is approved and plan is active, I walk your beneficiaries and/or emergency contacts through the process personally.

How fast can I get covered?

Some policies approve in 24-48 hours. Others take a few weeks depending on the carrier's underwriting. I'll give you a real timeline once we know which option fits your situation.

Do I need to pay anything today or give my payment info?

In most cases, no — payment isn't pulled until your policy is approved. Most carriers require your bank info when you apply to prove you have a verifiable method of payment. If a specific carrier's process works differently, I'll tell you upfront before you apply.

Why shouldn't I just wait to get coverage?

Two things work against you the longer you wait — your age and your health. Both affect your rate and what you qualify for. The coverage available to you today may not be available at the same price — or at all — next year.

Is there a deadline to apply?

Not necessarily — your health is the real deadline. Rates and approvals are locked in based on where your health stands on the day you actually apply, not when you first thought about applying.

What if I'm not ready to decide?

No problem. Getting a quote doesn't commit you to anything — that's the whole point of the conversation. Knowing your numbers now means you won't find out later that waiting costs you a whole lot more.

Quick Links

Connect With Bradley

© Easy Insurance Group. 2026. All Rights Reserved. Easy Insurance Group is a marketing name used by Bradley Vazquez, a licensed insurance producer (NPN: 21560803). Insurance products discussed or offered through this website are sold by Bradley Vazquez in his individual licensed capacity, not by Easy Insurance Group as an entity. Bradley Vazquez is licensed to sell insurance in AL, AZ, AR, DC, DE, FL, GA, IL, IN, IA, KY, LA, MA, MI, MS, MO, NE, NV, NC, OH, OK, PA, RI, SC, TN, TX, UT, VA, WA, WV, WI, WY. Not all products are available in all states. This website is for general informational and marketing purposes and does not constitute an offer to sell insurance in any jurisdiction where such offer would be unlawful.